Stablecoin Banks as the Next Trillion-Dollar Opportunity: Regulatory Pathways to a Banking Licence

Paul Joe (@0xPeejay, Investment Associate at Lyrik Ventures) and I co-wrote this article based on our discussion about the regulatory challenges facing stablecoin banks. You can stay updated with stablecoin industry news through his weekly Stablestats Dispatches or check out his latest project, stablestats.xyz, a comprehensive tracker for all stablecoin-related analytics.

The Trillion-Dollar Opportunity in Plain Sight

Among the more compelling investment theses in the blockchain space is the "stablecoin bank," a regulated financial institution built on token-native rails. At its core, a stablecoin bank issues and manages fully backed stablecoins while offering deposit accounts, payments, and other banking services to retail and institutional customers. The potential market is immense, promising to capture a significant share of the multi-trillion-dollar global payments and deposits landscape by offering faster, cheaper, and more programmable financial services.

However, many founding teams pursuing this opportunity significantly downplay the formidable regulatory challenges. While they excel at building sophisticated technology, they often underestimate a critical reality: to service retail customers with deposit-like products, a banking license is not an option, but an inevitability. The path to acquiring one is fraught with complexity, political risk, and intense scrutiny, a journey that requires as much regulatory strategy as it does technical innovation.

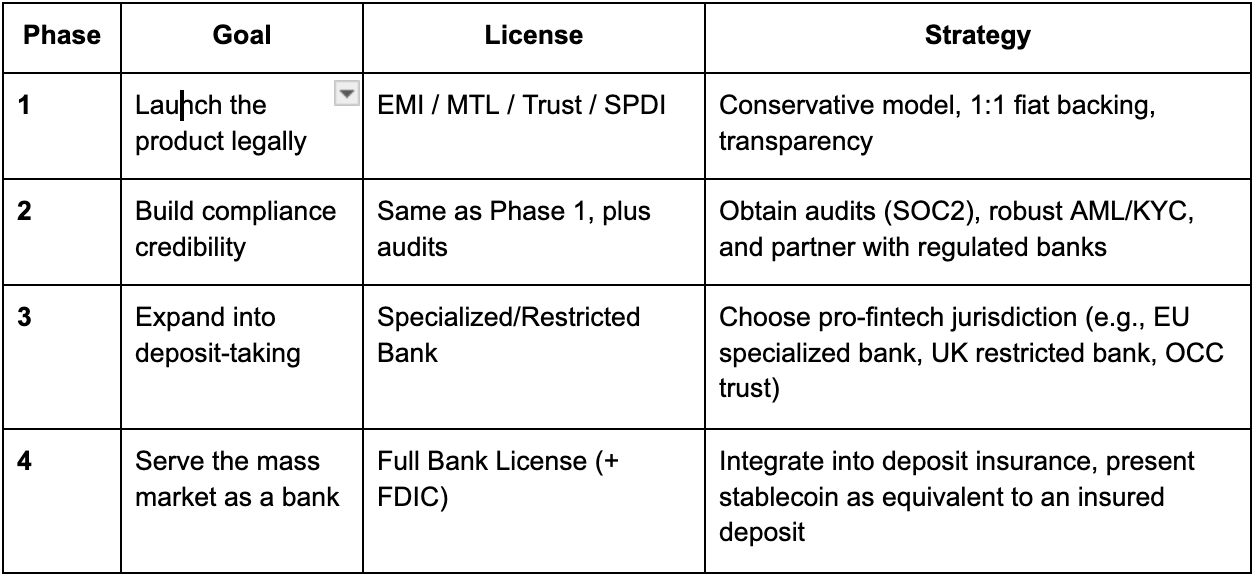

The Playbook: A Phased Approach to Becoming a Bank

The most viable path for a stablecoin issuer to become a fully-fledged bank mirrors the strategy successfully employed by neobanks like Revolut and Monzo. A critical lesson from their journey is that they didn’t need to change the rules; they needed to prove they could fit into existing ones. Success came from exploiting regulatory flexibility, demonstrating capacity, and making deep operational investments in compliance. As the history of neobanks shows, Revolut and others didn’t “become banks” overnight. They used lightweight licenses to grow fast, built compliance under pressure, and gradually migrated to full banking status as trust and capital allowed. This gradual, multi-phase journey is designed to build trust and progressively earn regulatory buy-in.

Phase 1: Establish a Regulatory Foothold

The journey begins not with a full banking charter, but with a lighter, more accessible license. Most neobanks, including Revolut and Monzo, started with Electronic Money Institution (EMI) or Payment Institution (PI) licenses. These were easier and faster to acquire. They allowed them to launch products, issue payment cards, and handle customer funds (though not lend against them), building a user base while navigating the longer path to a banking charter.

Common Starting Points:

E-Money Institution (EMI) License: Popular in the EU and UK, this license allows for holding client funds and processing payments. Revolut’s EMI license meant customer funds had to be safeguarded in accounts at real banks (Lloyds and Barclays) since Revolut wasn’t a bank yet.

Money Transmitter License (MTL): The state-by-state standard in the U.S. for payment companies. Circle initially operated under state licenses and was the first company to receive a New York BitLicense.

State Trust Charter: A more robust U.S. option (e.g., Paxos in New York) that permits custody and asset management, providing a higher degree of credibility.

Special Purpose Depository Institution (SPDI): Wyoming's crypto-native charter, designed specifically for digital asset banking. Kraken exchange obtained an SPDI bank charter in 2020, which lets it custody digital assets and hold fiat deposits with a 100% reserve requirement.

Phase 2: Build Institutional Credibility and Partnerships

With an initial license secured, the focus shifts to demonstrating institutional-grade compliance and risk management. Regulators will scrutinize the ability to manage risks like money laundering, operational security, and asset custody. To offer deposit-like features and other services beyond their initial license, many neobanks partnered with traditional banks. For example, Revolut partnered with Lloyds and Barclays in its early days, while Chime in the U.S. worked with FDIC-insured The Bancorp Bank and Stride Bank to hold customer deposits and provide banking services behind the scenes. For a stablecoin bank or issuer, this phase might involve securing SOC 2 and ISO certifications, undergoing rigorous audits to prove 1:1 reserve backing and security of funds, hiring seasoned compliance officers (often ex-regulators or banking veterans) to run AML/KYC programs, and partnering with established, regulated banks (like Circle’s use of BNY Mellon for custody of fiat reserves) to de-risk operations and signal legitimacy.

Phase 3: The Leap to a Restricted Banking License

Once the company has proven its model and compliance capabilities, it can apply for a specialized or restricted banking license. These charters are designed for new entrants and often come with lower capital requirements and a more limited scope of permissible activities. This was a key part of the neobank strategy. Revolut obtained a Specialised Bank License in Lithuania to passport services across the EU, and Monzo secured a restricted UK license in 2017 before upgrading to a full one.

Examples:

EU Specialised Bank License: Lithuania, for instance, offers a license that can be "passported" across the EU, granting access to the single market for deposit-taking and limited lending.

UK Restricted Banking License: This lets the institution call itself a bank and offer insured accounts on a trial basis (with a cap on total deposits of £50,000 during the mobilization phase), under close regulatory supervision.

U.S. National Trust Bank Charter: The OCC has granted conditional charters (e.g., to Anchorage) that recognize an entity as a bank for custody purposes, though not for deposit-taking from the public.

By Phase 3, the company is effectively operating as a bank in a limited capacity. This is a probationary period to demonstrate safety at a small scale.

Phase 4: Securing a Full Banking Charter

This is the final and most challenging step. Achieving a full banking license, complete with deposit insurance (like FDIC in the U.S.), unlocks the ability to serve the mass market and reframe the stablecoin as a fully regulated, tokenized deposit, once it meets all requirements of a standard bank in terms of capital, risk, and compliance. A full banking charter means the institution can offer the complete suite of banking services: taking insured retail deposits, making loans, and directly accessing central bank payment systems. It must also comply with banking laws, including adequate capital (possibly even higher than typical banks if required by regulators due to novel risks), liquidity ratios, rigorous board and governance structures, and adoption of deposit insurance. By this point, the regulator’s comfort is earned not just by compliance on paper, but by the institution’s track record. The phased approach builds a history: years of operations with no major compliance failures, transparent audits of reserves, and constructive engagement with regulators to create an environment where granting a bank license becomes a logical next step, not a leap of faith.

Summary Pathway to a Stablecoin Bank License

Unique Challenges on the Stablecoin Path

While the neobank playbook provides a map, stablecoin issuers face unique and heightened challenges that make their journey significantly more arduous.

Intense Regulatory and Political Scrutiny: Stablecoins are politically sensitive. Regulators harbor deep-seated fears of systemic risk, shadow banking, and the potential for digital bank runs, fueled by collapses like Terra/Luna and the political backlash from Facebook's Libra project. The only viable strategy is radical transparency and a conservative, "boring" approach focused on stability and 1:1 backing with fiat or government bonds.

A Higher Bar for AML/KYC: Regulators remain deeply skeptical of the crypto industry's ability to combat money laundering. A stablecoin bank must over-invest in its compliance stack, adopting best-in-class transaction monitoring tools (e.g., Chainalysis, Elliptic) and hiring seasoned compliance professionals, often from the regulatory world.

Resistance from the Incumbent System: Traditional banks often view stablecoin issuers as an existential threat and may lobby regulators to create a hostile environment. To counter this, successful stablecoin banks will likely start by focusing on enterprise or cross-border settlement use cases where they are not directly competing with retail banks, only moving into the consumer market after establishing a solid foundation.

The Impact of Incoming Regulation: A Double-Edged Sword

Incoming stablecoin regulation is likely a net positive for serious, well-capitalized teams. It will professionalize the space, create a regulatory moat, and sideline non-compliant competition.

The Upside (Increased Chance of Success):

Regulatory Clarity: Frameworks like the EU's Markets in Crypto-Assets (MiCA) regulation provide a clear, harmonized pathway for licensed banks or EMIs to issue "E-Money Tokens" (stablecoins). This removes ambiguity as serious projects know what licenses to pursue and how to structure their coin. It unlocks mainstream adoption as institutions will be more comfortable using a stablecoin under a regulatory framework.

Legitimization: Regulation formally recognizes stablecoins as a legitimate financial instrument, making integration with the traditional banking system easier. For example, once Circle’s USDC had reputable oversight and monthly reserve attestations, it partnered with Visa to enable USDC payments on Visa cards.

Competitive Moat: The high compliance bar (capital requirements, auditing, legal) will filter out fly-by-night players, leaving a smaller field of well-funded, institutionally-minded competitors.

The Downside (Increased Barriers to Entry):

Deposit Classification: Regulators may classify all stablecoins as deposits, forcing issuers to obtain a full banking license from the outset, a prohibitively expensive and slow process. Even if phased approaches are allowed, treating all stablecoin funds as deposits could invoke strict requirements like deposit insurance, which most startups can’t get without years of operation. In short, regulation could effectively force the stablecoin model into the arms of traditional banks, a huge barrier to new entrants.

Bank-Favoring Rules: Some proposed legislation explicitly limits stablecoin issuance to existing, insured depository institutions, which could lock out new entrants entirely. Other proposed regulations might prevent competition with traditional banks, such as prohibiting stablecoins from paying interest.

Fear of "Big Tech": Concerns over large technology companies entering finance and issuing currency could lead to preemptively strict rules that stifle innovation. For instance, MiCA includes criteria to designate a stablecoin as “significant” if the issuer is a central tech platform. A “significant” stablecoin faces extra scrutiny and oversight, implying that tech platforms that already have billions of users (like Facebook, Google, etc.), will face higher hurdles to launch a stablecoin. This can stifle innovation by treating even small projects with an outsize level of caution.

A Caveat for DeFi-Native and Algorithmic Models

It is crucial to note that incoming regulation is potentially a net negative for DeFi-native and algorithmic stablecoin propositions. Global regulators are coalescing around a model that demands simple, 1:1 backing with highly liquid, traditional assets like cash and short-term government debt. Algorithmic models, which rely on complex code and market incentives to maintain their peg, are viewed as opaque, inherently fragile, and a source of systemic risk.

These projects will face significant hurdles, including limited-to-no viable regulatory pathways, pressure to centralize their operations, and restricted access to the traditional banking rails required for redemptions. For these teams, a strategic pivot is essential. Viable options include:

Reframe as an Infrastructure Layer: Instead of issuing a regulated stablecoin, pivot to providing the underlying technology or protocols to licensed banks and issuers.

Partner with Licensed Entities: Integrate their technology into a fully compliant stablecoin framework offered by a regulated partner.

A Cautiously Optimistic Outlook with Compliance as a Differentiator

The creation of a stablecoin bank represents a foundational shift in financial infrastructure. The potential to build a more efficient, accessible, and programmable financial system is undeniable. However, success in this domain will not be defined by technological innovation alone, but by a deep and authentic commitment to regulatory compliance. A stablecoin bank that achieves a full license and public trust essentially creates a new class of banks that straddles traditional and digital finance. Its “deposits” can flow as tokens on any blockchain, enabling use-cases from global remittances to DeFi integration while being as safe as money in a vault.

For investors, the key is to back teams who view regulators not as adversaries, but as partners. The founders who succeed will embrace the rigors of the banking system and build their companies on a bedrock of trust, transparency, and institutional-grade compliance. If handled well, this wave of innovation will not just create immense enterprise value, it will redefine the very nature of banking for generations to come.

If you liked this article and are reading it on the web or received it from a friend, please consider subscribing to my regular newsletter (so you’ll get articles like this delivered fresh to your inbox) by clicking the subscribe button below.

| A guest post by |

This is a good primer for foundational play. Thank you.